Servicios Personalizados

Revista

Articulo

Español (pdf)

Español (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Accesos

Accesos

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkEconomía Coyuntural

versión impresa ISSN 2415-0622versión On-line ISSN 2415-0630

Revista de coyuntura y perspectiva vol.2 no.1 Santa Cruz de la Sierra 2017

ARTÍCULOS ACADÉMICOS

Financial speculation, global crisis and food sovereignty

Eugenia Correa* Wesley Marshall* Alfredo Delgado*

* A preview version of this paper was presented at The Critical Development Studies (CDS) Network. Conference, August 13-15, 2009. Zacatecas, Mexico. The authors thanks to DGAPA-UNAM, and also the anonymous readers of the Journal.

Recepción: 06/12/2016 Aceptación: 30/01/2

Abstract:

The process of economic and financial globalization has for decades established global economic structures that have left Latin America and other regions of the world highly vulnerable to the ebb and flow of the US economy. Mexico is an exemplary country in the region, by strictly following the practices of neoliberal globalization, and it became particularly dependent on food imports. This paper will focus on food prices and financialization. On the one hand, it will highlight the fact that Mexico has lost control over the supply and the price of its food, a similar phenomenon to the loss of other strategic sectors of its economy as energy. On the other hand, the paper emphasizes the speculative nature of the formation of commodity prices in international markets. The financialization of the economy is explored as complex phenomena, which has significantly altered the world's pricing system, with financial markets, exercising a considerable influence, therefore undermining the orthodox notion of determination of prices based on supply and demand.

Keywords: Financialization; Food Crisis, Commodity Prices

Clasificación JEI: F2; F3; L1.

Introduction

Much like many people labeled the onset of the financial crisis during the summer of 2007 as a "Minsky moment", many have treated the global food crisis that sparked international concern shortly thereafter as a "Malthusian moment". Minsky gained notoriety as one of the few modern American scholars to argue that modern finance carries with it inherent contradictions that lead to financial crises, such as the notion that the dynamics created during moments of financial calm in themselves cause financial fragility, which may lead to crisis. Malthus, on the other hand, was one of the classical economists that earned the field of economics the name of the dismal science, essentially proposing that while human population could grow exponentially, food production could not, and therefore, hunger would be a constant for humanity.

History has proven Malthus's conclusion to be correct, but his core hypothesis that economic forces or even economic laws determined this conclusion is, in our view, incorrect (Hodgson, 2004). There is no economic law or technical reason that condemns humans to hunger. In the same vein, we do not believe that the food crisis is the result of imbalances in supply and demand. We certainly do not deny that there is a greater demand for food than there is supply, and we also recognize that policies such as corn-based ethanol production have further limited the supply of world grains destined towards human consumption. However, our hypothesis is that sharpening of the historic food crisis, particularly in relation to the high amount of volatility in grain prices, is due to the various manifestations of financialized capitalism and not to a lack of ability for the world food production to adequately feed all humans.

Our paper is divided in various sections. First, we will examine how for years, the financial globalization has affected the functioning of non-financial firms (Serfati 2009; Lazonick 2013). In this section, we emphasize the concentration of producers into large firms, mostly transnational, with greater abilities to determine prices and levels of production as a dynamic that has dominated on a worldwide scale. Second, we will focus on the increasingly close relationship between the largest global food producers and the largest financial actors, and will argue that the recent volatility and rise in the cost of basic grains is due to the ebbs and flows of speculative capital rather than fundamental changes in the supply and demand of food. The third part of the paper will focus on the specific case of Mexico, which offers a revealing confluence of the first two factors. The opening of trade and the dismantling of state firms have decimated many of Mexico's productive sectors, notably for this paper in the agricultural sector. The remaining dominant players in the Mexican food production industry have established an oligopolistic position in the market, and along with their close allies in the country's financial sector, have established oligopolistic prices in the country.

2. Financialization and structural changes in the global economy

Starting in earnest with the rupture of the Bretton Woods monetary agreements in 1971, the worldwide economy has transited from a structure based on productive activity divided fairly clearly along national borders to a structure based on financial activity concentrated in a small handful of financial centers that have determined the recent evolution of economic events in much of the world. Accompanying, and in many ways permitting the shift towards financial globalization was the demise of the state as a promoter and regulator of economic activity, giving way to trade and financial opening that has greatly favo red the activities of trans-national corporations (TNCs). Much like the financial centers to which they are close linked, TNCs are highly concentrated in the same small handful of countries and have come to dominate strategic sectors of many economies.

However, a fundamental aspect of what has recently been denominated, as the financialization of the economy is that corporations that operate within productive sectors, such as manufacturing or food production, als o have come to be dominated by financial interests. As Guttmann and Serfatí (Guttmann, 2009; Serfatí, 2009) point out, the fact that the vast majority of the world's largest corporations are publicly traded has led to the phenomenon of shareholder maximization, in which owners of company stock seek short term gains in share prices over other considerations. As Serfatí states, shareholder maximization has directly and substantially eaten away at core activities of productive firms, such as research and development. As such, many productive companies have essentially turned into hedge funds that as a side business sell food, cars, etc. This fact is highlighted by the ownership structure of emblematic US companies such as GM, Chrysler, Sears, and GE among others, and their respective fates. Not only is the destiny of these companies decided by financial decisions to a much greater degree than the quality of their products or their demand for it, but they have also established much closer relationships to the world's largest financial firms.

As such, after three decades of financial globalization, the world's economy can be classified today as financialized. Within this regime of capital accumulation, the world's largest financial conglomerates strongly and directly contribute to the determination of prices and levels and qualities of economic activity. Indirectly, these same groups are also a significant determining factor in the activities of corporations operating in productive sectors. While decades ago, the fate of banks such as Citibank and Goldman Sachs would have had a relatively insignificant impact over food production and manufacturing activity, the destinies of these banks and food production and pricing are so closely interwoven that the food crisis cannot be explained without analyzing its genesis in the global financial crisis.

Before the outbreak of the global crisis, clearly demonstrated by the wild swings in grain prices. At its highest point at the middle of 2008, the wheat reached the 450 dollars by to, 250 maize and rice 750 dollars per ton (FAOStat). Very few academics and other experts had raised alarm over the grave consequences of structured finances, which have come to dominate the latest phase of finance led capitalism. Although some processes had given evidence of the fragility that derivative instruments produce, such as the bond crisis in the United States in 1994 (Borio and McCauley, 1995); the Asian crisis of 1997 (Kregel, 1998); the financial frauds of the Enron era (Aglietta, 2004); and the exponential growth of the credit derivatives (Liu, 2004). The same can be said for more theoretical-analytical studies, such as those focusing on structured finance's consequences on payments systems (Perold 1995), the risks of securitization in regards to financial stability, or financial frauds (Correa, 1998, Toporowski, 2000, Partnoy, 2003).

The new dynamics in financial markets that encapsulated the last 30 years of economic transformations were incorporated into academic analysis through thematic studies including the external debt of the developing countries and the 80s debt crisis; the developing countries' external debt

securitization and the Baker and Brady Plans; and the analysis of the financial globalization of the nineties, while the authors of the regulation school coined the concept of finance capitalism or finance led-capitalism or financialization (Chesnais, 1996, Aglietta, 1998, Epstein, 2005, Serfati, 2009, Guttmann, 2009).

This global financial crisis was within the theoretical universe of the regulation theories (De Bernis, 1988) and Postkeynesian analysis, as deeply analyzed in Minsky works (Minsky, 1982) Although instability and financial crises were largely studied from this school of thought, the development of structured finances did not provoke modifications to their studies until very recently (Epstein, 2005, Wray, 2007). Nevertheless, Minsky (1987) warned about securitization:

"Securitization implies that there is no limit to bank initiative in creating credits for there is no recourse to bank capital, and because the credits do not absorb high-powered money [bank reserve]."

The monetarist fight against inflation created the market trends towards securitization:

Securitization reflects a change in the weight of market and bank funding capabilities: market funding capabilities have increased relative to the funding abilities of banks and depository financial intermediaries. It is in part a lagged response to monetarism. The fighting of inflation by constraining monetary growth opened opportunities for nonbanking financing techniques. The monetarist way of fighting inflation, which preceded the 1979 "practical monetarism" of [thenFederal Reserve Chairman Paul] Volcker, puts banks at a competitive disadvantage in terms of the short-term growth of their ability to fund assets. Furthermore, by opening interest rate wedges, monetary constraint provides profit opportunities for innovative financing techniques...

Bank participation in securitization is part of the drive, forced by costs, to supplement fund income with fee income. The development of the money market funds, the continued growth of mutual and pension funds, and the emergence of the vast institutional holdings by offshore entities provide a market for the instruments created by securitization. (Minsky, 1987).

Securitization arose from the US market hand by hand with globalization, looking to add new profitable assets around the world at the disposal of rent-seeking institutional investment managers.

There is a symbiotic relation between the globalization of the world's financial structure and the securitization of financial instruments. Globalization requires the conformity of institutions across national lines and in particular the ability of creditors to capture assets that underlie the securities. (Minsky, 1987).

In 2007, the subprime crisis soon reached other assets with high quality mortgage backing and to other securities linked to car loans and credit cards, as well as other structured finance products such as CMBs, CDOs and CDSs. The deregulated securitization had created an opaque, fragile and disproportionate financial order, operating in volumes never before seen, out of reach from the central banks' and the government regulators' control, and with amounts well in excess of the entire volume of worldwide production and trade.

The financial crisis reached one of its most difficult stages at the end of 2008 although it should not be forgotten that starting in 3Q 2007 a great increase in episodes of severe credit constraints and bankruptcies had occurred. Beginning with particular force in 2007, the toxic assets in the portfolios of the special purpose vehicles of Citigroup and others large banks began to lose money. Thus, although the bankruptcies of Lehman Brothers and the collapse of AIG in September of 2008 triggered the worst episode of credit constraint until now, the argument that the entire financial crisis arose from the "mistake" of the American government to let Lehman go bankrupt is not valid.

The globalization of structured finance explains the magnitude and depth of the financial crisis, which was born in the US mortgage stock market. Structured finance relates to the combined action of the instrumental and operative innovation that changed the basic operation of the financial markets. Thus, structured finance incorporates all processes of credit securitization and the rebirth of derivative instruments in the 80s and the credit derivatives of the 90s, which became what the literature now denominates the shadow banking system, with the creation ex profeso of financial organizations like the special purpose vehicles or monoline insurers, or preexisting ones like hegde funds, mutual funds, investment funds, funds of funds, investment banks, etc. Others fundamental actors in the explosion of structured finance include the rating agencies, which evaluate opaque instruments without markets or with a very restricted ones.

Structured finance was a powerful backer of financial deregulation and liberalization, creating markets all around the world through credit expansion, generating very lucrative financial activities. This globalized financial market, in spite of the large number of participants in the different segments of the market, is supported by a small number of large financial conglomerates, which have recently experienced successive and significant writedowns and capital losses. The crisis arose because the fall in the prices of the assets backed by real estate, and later many others, but also because of the reduction in the market liquidity on which the expansion of securitization depends.

At this point, it no longer mattered how fast the central banks reacted in lowering interest rates, but rather on the quantity of securities, even those losing price and market, that they would accept for purchase or collateral (or how much was financially and politically feasible) Nevertheless, as was noted for more than 15 years by diverse scholars, due to the volumes of assets created by structured finance and the intrinsic opacity of its operations, the actions of central banks in the face of a systemic crisis is extremely limited.

From the first crises generated by derivative operations at the beginning of the 90s, like Procter and Gamble, or Orange County, financial authorities have faced such problems by lending funds and trying to cajole large financial conglomerates operating in the Over the Counter (OTC) derivatives market to put into operation measures of self-control and self-supervision. In spite of the magnitude of the current crisis, debates over market restructuring and regulation still focus on the same ideas of liquidity support and furthering self-regulation.

The financial crisis has greatly reduced significant segments of structured finance's activities, and it is not yet clear how the world's financial systems will be able to be reformed. The huge and growing area of financial operations that were unlocked by structured finance continues in several of its segments, at least for now, as several of their segments continue to capture resources that are help alleviate, albeit partially, the insolvency that became generalized in Q4 2008 and Q1 2009. Sources of funding include the margins on interest rates; government budgets; workers' pension funds; rising labor productivity; the reduction in workers incomes; the increasing exploitation of natural and energy resources; and the renewed speculation in the traditional business of arbitrage in commodities and currencies.

3. From financial crisis to food crisis: Price determination via global speculation

The food crisis is part of these changes in financial markets and securitization, which reached a new stage when financial innovation, albeit damaged by the crisis, led to a new type of instruments based on commodities, with the peculiarity of becoming portfolio investments for institutional investments and diverse investment funds.

According to Masters "...Institutional Investors are one of, if not the primary, factors affecting commodities prices today. Clearly, there are many factors that contribute to price determination in the commodities markets.." (Masters, 2008). The high volatility of the food prices could be illustrated by the behavior of the price index estimated by FAO (2016) since the sharpest moments of the financial crisis 2007, see the Graph 1.

The transformation of institutional investor's behavior is the root cause of the rapid increase in commodity speculation. Goldman Sachs and other investment banks place financial instruments backed by commodity price indexes in financial markets not as a hedge for the exchange of commodities in a determined moment, but as instruments that will stay on investors' balances in the hope of increasing their value. Master states that "Index Speculators, allocate a portion of their portfolios to "investments" in the commodities futures market, and behave very differently from the traditional speculators that have always existed in this marketplace. I refer to them as "Index" speculators because of their investing strategy: they distribute their allocation of dollars across the 25 key commodities futures according to the popular indices the Standard & Poors - Goldman Sachs Commodity Index and the Dow Jones AIG Commodity Index"

After the 2000-2002 crises, institutional investors found in the creation and maintenance of these instruments on their balances a way to grow and maintain high levels of profits among investors, even in spite of the difficulties that companies and production in general continued facing.

"Commodities looked attractive because they have historically been "uncorrelated," meaning they trade inversely to fixed income and equity portfolios. Mainline financial industry consultants, who advised large institutions on portfolio allocations, suggested for the first time that investors could "buy and hold" commodities futures, just like investors previously had done with stocks and bonds." (Masters, 2008)

As such, in 1998, less than 150 billion dollars of instruments based on commodity indexes were exchanged, whereas this figure reached 260 billion dollars in march of 2008.

In the light of such information, a transcendental consideration revolves around why a derivative contract based on an underlying asset contributes to the determination of its price. According to conventional theory, there is a supposed convergence between future prices and current delivery prices, and when the maturation date of a future contract nears, the price of the future tends to converge towards the current delivery price of the underlying asset. Upon maturation, the price of the underlying asset is close to or equal to the delivery price. According to theory, this convergence allows markets, particularly financial markets, to be more efficient.

Based on this vision, three scenarios become probable. The first is that the future price is higher than the delivery price during the probable date of delivery. When this occurs there is a clear opportunity for arbitrage, in the form of the sale of the future contract, the purchase of the asset, or the transfer of the asset. As such, a series of benefits equivalent to the difference between the future and delivery price can occur. As operators take advantage of this condition, the future price will diminish.

The other scenario is that the future price is below the delivery price during the probable date of delivery. In this scenario, companies that are interested in acquiring the asset will purchase the future contract and wait for its delivery. In this case the opposite of the anterior scenario will occur, and the future price will tend to rise.

The last scenario is that the future price approaches the delivery price during the delivery period, and as such, the prices of both markets converge. For authors such as Hull (2002) and Jarrow and Turnbull (1996), this would be due to the fact that speculators do not deal in futures contracts unless the expected gains are favorable; to the contrary, those who hedge can expect losses due to the benefits of the minimization of risks that they obtain through a futures contract. This is to say that if more speculators hold long positions than short positions, there will be a tendency for the future price to be lower than the expected delivery price. But in the opposite case, the tendency of the future price would have to be greater than the expected future delivery price.

However, to the contrary of what the conventional literature puts forth, this is not the case. Fundamental to the growth of the derivatives market is speculation. If prices did in fact converge, there would be no room for speculation or for derivatives for that matter. Rather than proposing a convergence of prices, it is more apt to speak of a determination of financial and non-financial asset prices by a large number of derivative contracts managed by a small number of institutional investors that contribute in a fundamental way to the establishment of price levels.

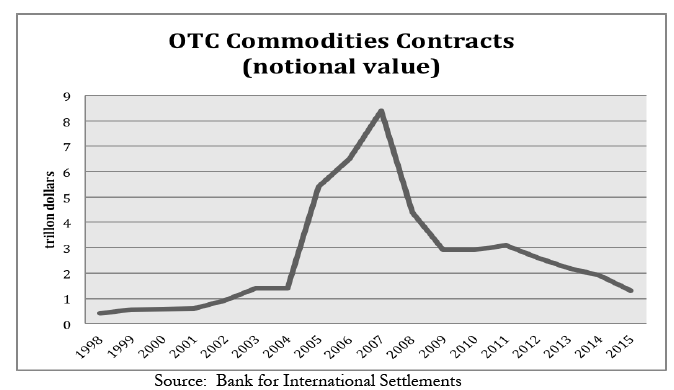

The volume of resources negotiated in the derivatives market (in this case speaking of the OTC market for commodities, which includes agricultural and energy products, among others) shows a sharp increase in the number of negotiated contracts precisely before the great crisis, as can be seen in Graph 2. The data reflect the level of speculation in derivatives markets. In 2007, 8.4 trillion dollars were negotiated via OTC commodity contracts, but it is beginning in 2002 that the upward tendency in the value of negotiated contracts can be seen, which coincides with the rise in current delivery prices of agricultural products seen during 2006-2007. Upon analyzing the behavior of current delivery prices for agricultural prices such as corn, a strong increase can be seen in 2006 and 2007, coinciding with the increase in the OTC commodities contracts in the same period. And if the prices of the corn futures market in the Chicago board of trade are analyzed, there is a clear increase in the price of contracts negotiated beginning in June of 2006, which is to say that there is a causal relationship between the futures market and current delivery prices.

According to the Trade and Development Report (2008) "...future prices are one of the determining criteria of current delivery prices" (UNCTAD, 2008). The Institute for Agriculture and Trade Policy stated in January 2009 report that price speculation is a fundamental factor in the increase in delivery prices, and that according to estimates made by CBOT consultants, 31% of the increase in corn prices was due to the pervasive financial speculation, independent of the fundamental factors of market supply and demand.

The derivatives market has strongly contributed to the modification of the behavior of current delivery prices as can be observed statistically and as reflected in the reports presented by authorities and international organisms. The problem is based on the formation of a speculative bubble in agricultural products in the derivatives markets that reached staggering proportions in 2006 and 2007, provoking profound effects in the real economies of many countries.

Yet the effects of the increase in food prices have had very different effects. First, many developing countries are exporters of raw materials and food, and the surpluses generated imply an improvement in the terms of exchange. However, a significant part of these surpluses is, in fact appropriated by the exporting corporations that include segments of local oligarchies, as well as TNCs in the sector and especially funds invested in speculative instruments. On the other hand, countries that import food, and sectors of low income in both countries that are net exporters and importers suffer from the rise in food prices, which have not translated into generalized increases in salaries, and as such, an enormous social group has been creating in southern countries with little to no access to minimal levels of nutrition.

As stated by the UNCTAD, "... high prices for basic products have positive and immediate effects on economies in development and in transition that export them, given that income from exports has risen. At the same time, this increases the potential for funding new investments in infrastructure and productive capacity that are necessary to advance processes of diversification, structural change and an expansion of economic activity and employment. Whether or not countries can take advantage of this situation depends on the distribution of the income from the export of basic products among national and international interest and the destination of this income than exporting countries can retain" (UNCTAD:19).

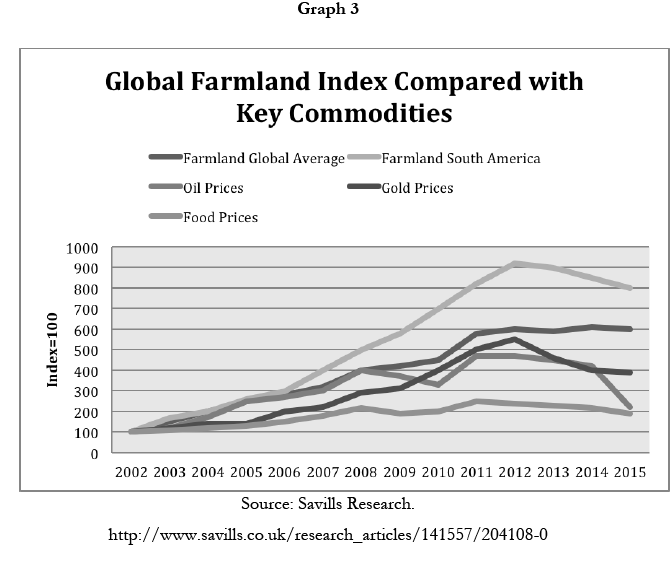

However, the increase in food prices based on the expansion of financial corporations (Lazonick, 2013, Serfatí, 2013) put a significant part of the economic surplus towards the financial markets themselves. The strength of financial growth can strengthen investment capital flows, but it can also become an inflationary increase in the price of the underlying assets. Through this dynamic we can see an increase in the price of agricultural land that has been well above the increases in the price of many commodities, including oil or gold, as seen in Graph 3.

The great crisis of 2007 gave a strong impulse to the increase in international credit, which has reinforced an inflationary bubble in the prices of not only of food and commodities, but also of agricultural land, especially in in South America and Eastern Europe. A part of this inflationary bubble in agricultural land is linked to the growing expectations of profitability of the crops dedicated to bioenergy. However, the very expansion of the securitization of land and water and the expectation of profitability of all this, expands credit capacity and exponentially accelerates the prices of these assets.

4. The Case of Mexico: price determination via domestic market structure.

While the fixation of worldwide commodity prices in financial markets has far reaching effects on all countries, there are also important domestic components of the food crisis that differ among countries. In this section, the particular case of Mexico will be examined. Although there are many similarities between Mexico's experience and those of other countries in the developing world, the space for comparative analysis will be limited.

Over the last few decades, Mexico has been one of the most faithful adherents to the spirit and letter of Washington Consensus (WC) policies, which have favored trade and financial liberalization and the reduced role of the state in economic activities. Mexico is also a noteworthy case in the scope and depth of its free trade agreement with the US and Canada (NAFTA). As has been the case with all other countries that have adopted WC policies, Mexico's economy has become ever more dependent on external financing while its national productive apparatus has withered. Unlike other large economies in the region such as Brazil and Argentina, however, in Mexico the agricultural sector has been particularly hard hit.

Due to the fact that much of Mexico's land is not arable and the distribution of a large part of arable land into small family and community owned tracts, even under the best of circumstances Mexico could never have developed into a major agricultural center during the last thirty years. However, while not possessing the Argentine pampa, Mexico can and should be self sustaining in terms of food production. However, the onerous conditions of trade and financial opening in Mexico have created a situation in which Mexico has lost its sovereignty in many terms, including in food production.

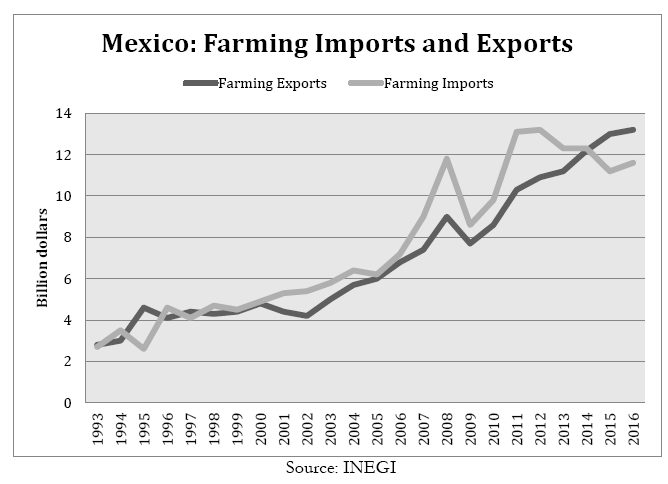

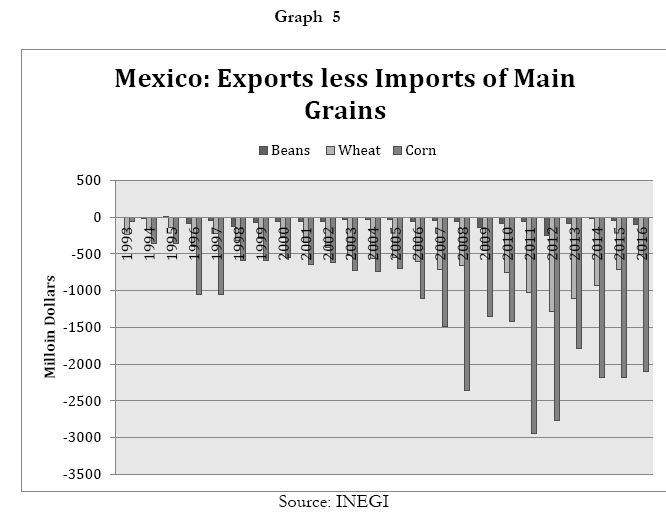

As has occurred in other sectors of the Mexican economy, the complete lack of centralized planning has created glaring contradictions, such as the fact that Mexico exports large volumes of crude oil but must import a large part of its refined gas for local consumption. In the case of the agricultural sector, Mexico exports more than it imports, yet the country remains highly dependent of the importation of grains, particular corn from the United States. These tendencies can be seen in the Graphs 3 and 4. The fact that agricultural products that are more profitable for exportation have crowded out the corn production necessary for local consumption constitutes one of the reasons for which Mexico has been particularly negatively affected by the current food crisis.

Yet Mexico's agricultural capacities have not merely shifted focus; they have also become significantly reduced. During the decades following the Great Depression, the system of publicly-owned banks established in Mexico permitted the development of several of the country's economic sector. However, after the debt crisis of 1982 and the adoption of WC policies, the activities of such banks were greatly reduced, if not entirely eliminated. As has occurred many times, publicly owned banks that serve traditionally credit starved sectors of the economy were wound down so that more efficient private sector banks could enter into competition, but the end result was that such areas simply became, once again, financially underserved. With inadequate financial assistance from the state, most Mexican grain producers could never compete with the ever growing concentration of US agribusiness. And within the context of a decade long slump in grain prices, the trade opening under NAFTA, and a chronically overvalued peso, the capacities and output of domestic food production has fallen drastically.

However, under the conditions of contracting domestic output, there has also been a significant bifurcation of food production in the country. On the one hand, TNCs such as Bunge, Monsanto and Cargill have significantly increased their presence in the local market, while locally owned corporations such as Gruma and Bimbo have also greatly increased their market share within the country. Both types of companies have large scale international activities (the Mexican ones are often classified as Trans-Latinas), and both are fully integrated into the dynamic of financialization. Gruma, for example, is part of the same business group as Banorte, the largest domestically owned Mexican bank. With access to global foreign financial markets, and seeking greater financial gains rather than the fulfillment of the needs of the local economy, such TNCs have directed significant portions of their production to foreign markets.

On the other hand, the smaller grain producers that in the past had supplied the needs of local market have become ever more marginalized. With the recent full liberation of the corn and bean imports under the mandates of NAFTA, the two most important food items in the Mexican diet have become even more dependent on US imports. Even subsistence farming, a perennially fragile sector of almost all economies, has been strongly impacted by these changes.

What has emerged in Mexico is therefore a two staged pricing system, in which grain prices determined in financial markets of developing countries establish a base price for agricultural prices once they leave the farm, guaranteed by the hedge positions taken by government agencies such as ASERCA and PROCAMPO, which offer financing to agricultural producers; but due to the oligopolistic pricing system in the domestic market for processed goods, including tortillas, prices rise much further for the customer.

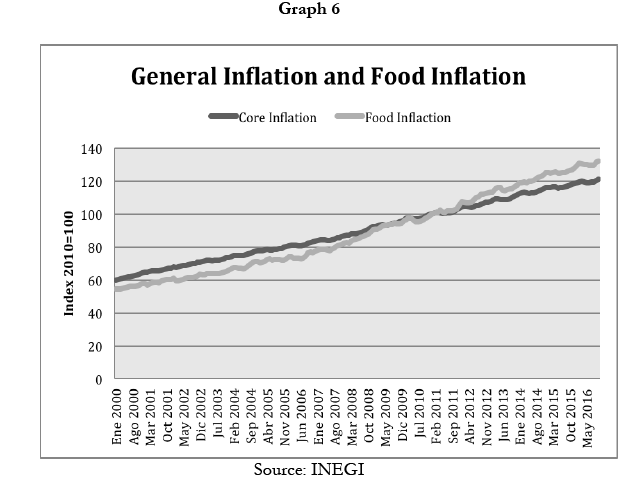

As can be seen in Graph 6, even after grain prices fell sharply off their highs in international markets, they have continued to rise in Mexico, outstripping the core inflation of which they form a part. Mexico therefore finds itself particularly vulnerable from food crises not only due to the fact that it does not produce all of the grain necessary to feed its population and therefore has to import grains at prices dictated by financial markets, but also due to the oligopolistic structure of its food production sector. This oligopolistic price formation has not changed even with the commercial opening created by the NAFTA, and explains to a substantial degree why food prices tend to remain above core inflation.

Mexico has become on one hand the country a huge importer of basic grains, with important consequences on the external commercial balance. On the other hand, the commercial opening, instead of protecting food prices from price increases through greater competition, has merely strengthened the oligopolistic agricultural sector and allow for extraordinary profits for domestic and foreign firms operating in the country, coupled with growing prices for the nation's consumers.

5. Conclusions

As has been attempted to show, while the expansion of the world's population has put pressure on food supplies, and while chronic malnutrition has plagued many countries for centuries, the current food crisis contains elements that are much more current and related to the dominance of financial activity in almost all aspects of the world economy. The dramatic oscillations in prices of the world's principal grains can be traced to the global financial crisis of 2007. Indeed, the capacity for counties to deal with the volatile conditions of the global economy depends greatly on historical tendencies and conditions, but also on the priorities of governments in power. Net exporters of grains have the unique opportunity to recycle windfall profits into greater investments for a diversified and dynamic economy, while economies that are historically dependent on food imports will have to be increasingly creative in finding ways to protect their most vulnerable citizens.

Mexico offers a clear case of a country that has not taken advantage of its natural resources to assure food sovereignty. The destruction of Mexican agriculture, coupled with the dependence of US imports and the entrenchment of oligopolistic food producers has created a situation in which the country's poorer citizens have been deprived of the most basic of goods to the direct benefit of national and international speculators and local producers, many foreign-owned, determined to maintain profits at all costs.

The Trade and Development Report from the UNCTAD (2009) confirms much of our hypotheses on the international level, highlighting the financial instability and the relatively novel use of commodity indexes as tools for widespread speculation, fuelled by financial innovation and derivatives trading as the principle driving forces of the sharp rises in commodity prices from 2006-2008.

With continuing financial volatility on the near horizon, the price of the world's principal grains can be expected to once again fluctuate significantly. Given the sensitivity of these prices to such a large segment of the world's population, governments will be greatly challenged to demonstrate their creativity and willingness to confront difficult situations to the benefit of their citizenry, as well as to justify past policies that in many cases, such as the Mexican, that have led their countries to positions of extreme vulnerability in the face of international crises.

References

Aglietta, M., A. Rebérioux (2004) Dérives du capitalisme financier, Ed. Albin Michel, Paris. [ Links ]

Borio Claudio, and Robert McCauley (1995) The anatomy of bond market turbulence of 1994, working paper 32, BIS, Basle. http://www.bis.org/publ/work32.pdf?noframes=1 [ Links ]

Chesnais, Francois (1996) La mundialización financiera. Génesis, costos y posturas Paris, Ed. Syros. [ Links ]

UNCTAD (2009). Trade andDevelopment Report. New York and Geneva. [ Links ]

Correa, Eugenia (1998) Crisis y desregulación financiera. Ed. Siglo XXI, México. [ Links ]

De Bernis, Gerard (1998). El Capitalismo Contemporaneo Editorial Nuestro Tiempo. Mexico. [ Links ]

Epstein, Gerald A. (2005) Financialization and the world economy, Edward Elgar Publishing. [ Links ]

FAO (2016) Fao Food Prices Index, http://www.fao.org/worldfoodsituation/foodpricesindex/en/ [ Links ]

Guttmann, Robert (2009) Introducción al capitalismo Conducido por la Finanzas en Ola Financiera, enero-abril. UNAM. [ Links ]

Hobsbawm, Erick (2009) Socialism hasfailed. Now capitalism is bankrupt. So what comes next?, The Guardian, 10 April. [ Links ]

Hodgson, Geoffrey (2004) Malthus, Thomas Robert (1766-1834). Biographical Dictionary of British Economists, edited by Donald Rutherford (Bristol: Thoemmes Continuum). [ Links ]

Jarrow, Robert and Stuart Turnbull (1996) Derivative Securities, South-Western College Publishing, Ohio, United States. [ Links ]

Kregel, Jan (1998) Derivatives and Global Capital Flows: application to Asia, Levy Institute, working paper, 246. [ Links ]

Lazonick, William. (2013) The Financialization ofthe U.S. Corporation: What Has Been Lost, and How It Can Be Regained, Seattle University Law Review,Vol. 36. [ Links ]

Liu, Henry (2002) Perils of Debt-propelled Economy, Asia Time on line, september 14. [ Links ]

Masters, Michael (2008) Testimony before the Committee on Homeland Security and Governmental Affairs United States Senate, May 20, http://hsgac.senate.gov/public/_files/052008Masters.pdf [ Links ]

Minsky, Hyman (1982) Can "it" happen again?, New York, Sharp. Minsky, Hyman (1987, 2008) Securitization, www.levy.org [ Links ]

Partnoy, Frank (2003) Codicia Contagiosa, Ed. El Ateneo, Argentina. [ Links ]

Perold, André (1995) The payment system and Derivative Instruments, working paper Division Research, Boston, Harvard Business School. [ Links ]

Serfati, Claude (2009) Globalization: An Unsustainable Trajectory. Paper prepared for the Coloquio "La crisis global y América Latina", 19-21 de enero. [ Links ]

Serfati, Claude (2013) La lógica financiero-rentista de las sociedades transnacionales, Mundo Siglo XXI, revista del CIECAS-IPN. N. 29, Vol. VIII. Pp. 5-21. [ Links ]

Taibbi, Matt (2009) "How Goldman Sachs has engineered every major market manipulation since the Great Depression" http://www.rollingstone.com/politics/story/28816321/thegreatamerican bubble machine [ Links ]

Toporowski, Jan (2000) The End ofFinance: the theory of capital market inflation, financial derivatives and pension fund capitalism. New York, Routledge. [ Links ]

Wade, Robert (2008) "Financial Regimen Change", New Left Review 53, September-October. [ Links ]